Pinduoduo: If You Must Invest In E-Commerce, Look Overseas (NASDAQ:PDD)

It goes without saying that e-commerce stocks are among the hottest sector to invest in this year. With the pandemic bruising the world and shuttering retail stores, the shift from bricks-and-mortar spending to online shopping has only accelerated this year.

The problem from an investors’ standpoint, however, is that most of the key U.S. e-commerce trades are already very overcrowded. Amazon (AMZN) stock has nearly doubled year to date. Etsy (ETSY), an arts-and-crafts vendor that a few years back the market had left for dead, has seen its shares triple as the company grew quickly in selling both housewares and masks. Even eBay (EBAY), long a laggard and struggling to remain relevant in the internet space, has seen its shares appreciate >40% this year.

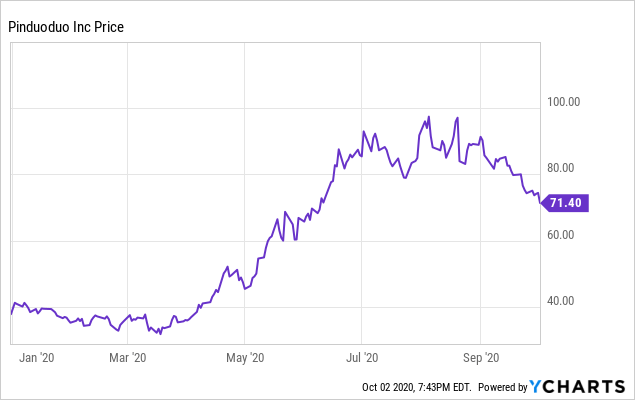

Here’s an e-commerce idea that many investors haven’t heard of, though: Pinduoduo (PDD). Now Pinduoduo has also seen its share of gains this year, up ~70% year-to-date, but in my view with the company’s tremendous growth and its dramatic improvement on profitability metrics this year, there’s a lot of upside left to go for Pinduoduo – especially as the stock is currently ~25% down from peaks near $100 reached in August.

E-commerce with a social twist

For investors who are unfamiliar with Pinduoduo, this is the second-largest e-commerce marketplace in China, behind the behemoth Alibaba (BABA) but ahead of JD.com (JD), which focuses primarily on electronics.

Pinduoduo’s “virtual bazaar” offers all manner of products, like Amazon. But where Pinduoduo distinguishes itself is that the company is a pioneer of the “social e-commerce model,” that mixes both shopping and social media.

There are two key aspects of this social commerce model for Pinduoduo. First, the company encourages and rewards organic word-of-mouth marketing because the company offers shoppers discounts the more friends that they bring into their purchase. When inviting at least one other person to buy the same item, both shoppers are rewarded with a discount. This is referred to as team purchasing in Pinduoduo – the company’s name translates to “together, more savings, more fun.” Pinduoduo is just the marketplace operator – in most cases products are shipped directly from manufacturers to the shoppers, which benefit from this model because they attract larger-volume orders.

The second key aspect is livestream shopping – a foreign concept in the U.S., but essentially one in which brand promoters livestream themselves discussing the product and draw in shoppers. An interview with a Pinduoduo employee on Medium discusses how this phenomenon is changing shopping in China:

The most significant shift in consumer behavior we see in China is the move away from the “search, pay and leave” model of legacy e-commerce platforms to a social commerce model such as Pinduoduo’s, which more closely mimics the offline shopping experience by integrating the serendipitous joy in finding great buys and the social interaction that shopping together brings.

Livestreaming ecommerce, for example, is increasingly becoming a preferred way to shop in China precisely because it is more interactive and social. We found that with livestreaming, consumers were more willing to purchase categories that traditionally did less well on e-commerce platforms. That is because being able to see and interact with the seller through livestreaming built trust and confidence in the products.”

These social features are the key drivers behind Pinduoduo’s growth, and how the company distinguishes itself from its much larger rival Alibaba.

Tremendous user and revenue growth

Needless to say, Pinduoduo’s growth has been explosive, and the onset of the coronavirus has only helped Pinduoduo sustain its massive growth rates.

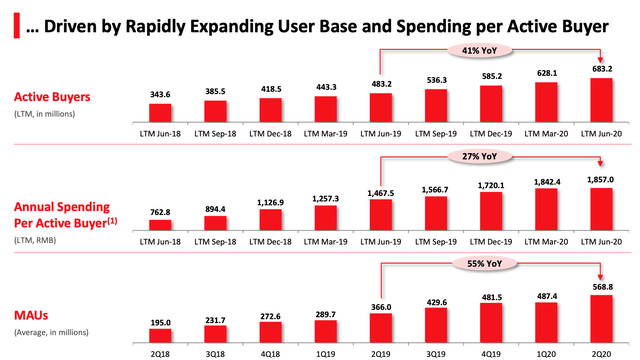

As seen in the chart below, Pinduoduo reached 683.2 million active buyers in the second quarter of 2020, up 41% y/y. This compares to roughly 742 million active buyers on Alibaba. Monthly active users saw even stronger growth at 55% y/y.

Figure 1. Pinduoduo user growth Source: Pinduoduo Q2 investor presentation

Source: Pinduoduo Q2 investor presentation

Perhaps even more impressively: average spend per buyer has also been trending steadily upward, showing that Pinduoduo has been able to generate loyalty and sticky buyer behavior.

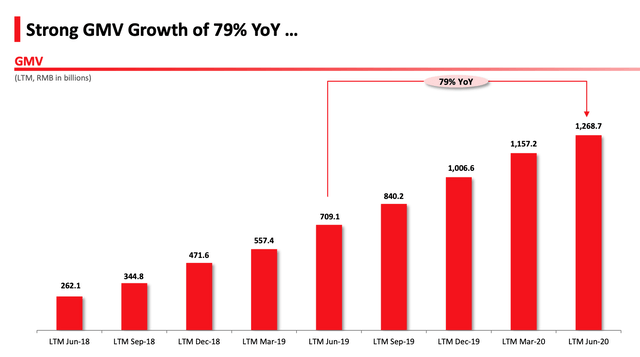

And despite having already reached a tremendous scale, Pinduoduo’s GMV (gross merchandise value, a measure of all the goods sold on its platform) is still growing at a rapid clip. As of Q2 of 2020, Pinduoduo saw GMV grow 79% y/y to RMB 1.27 trillion, which at today’s rate of RMB 6.79 to the dollar represents a dollarized GMV of ~$187 billion.

Figure 2. Pinduoduo GMV growth Source: Pinduoduo Q2 investor presentation

Source: Pinduoduo Q2 investor presentation

For comparison: Alibaba doesn’t report GMV every quarter, but in May reported $1 trillion in annualized GMV for the year ending in March 2020. Similarly, Amazon doesn’t report GMV, but third-party estimates put Amazon’s GMV at $335 million for 2019, at a ~30% growth clip.

At Pinduoduo’s much faster growth clip, there’s a lot of market share available for the company to take. As an aside here: Pinduoduo’s monetization rate, which is the amount of revenue it generates divided by its GMV, has stayed constant around ~3% since 2019 (at the time of its 2018 IPO, monetization was closer to 2.5%). As such, Pinduoduo’s revenue growth going forward will largely be proportional to its ability to expand GMV. For the following fiscal year, Wall Street analysts are expecting Pinduoduo to generate, in dollar terms, $10.98 billion in revenue – which would represent 54% y/y growth over 2020 consensus.

In terms of specific growth drivers for Pinduoduo – the company has long had a following among the rural communities of China that form the majority of the population, whereas Tmall’s focus on electronics and high fashion cater more to urban dwellers. The company has set out a strategy to capture more growth in the agriculture space, which is among the sectors that has been least touched by technology/e-commerce. David Liu, the company’s head of strategy, noted as follows on the Q2 earnings call (emphasis added):

One in four Chinese workers work in agriculture, but the industry makes them less than 10% of China’s GDP. This is because agriculture has lagged behind other industries in digitization […]

Pinduoduo is already one of the leading e-commerce platforms for agriculture. In 2019, we generated RMB136.4 billion or 13.6% of our GMV from agriculture produce and related goods […] 38% of our annual active buyers purchased in this category last year, with a 70% repurchase rate […]

We expect to continue gaining market share in agriculture and we see potential for our agriculture GMV to exceed RMB1 trillion in 5 years.”

The key point here is that Pinduoduo expects agricultural products alone to be almost the size of its current GMV within five years, and this is a space in which competitors like Alibaba have had much less traction.

Operating leverage

Perhaps even more impressive than Pinduoduo’s growth rates, however, is the fact that the company has been able to capitalize on that growth to generate operating leverage.

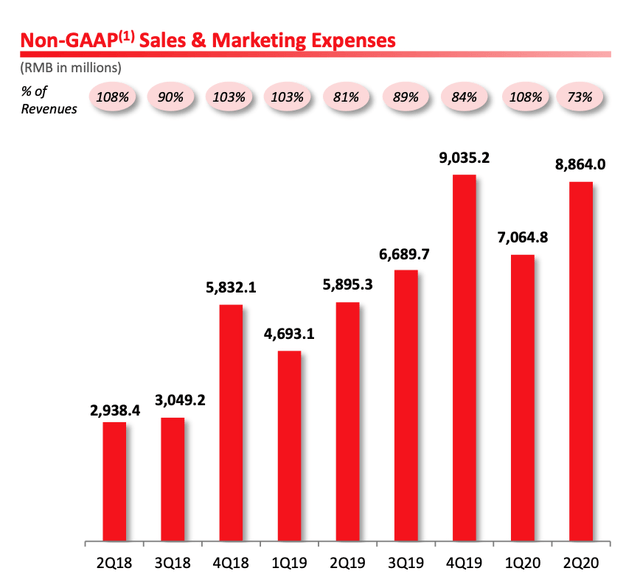

Like most technology companies, Pinduoduo’s largest expense category is sales and marketing. But due to its focus on “social shopping,” as Pinduoduo grows larger and more popular, it hopes to rely more on organic marketing instead of paid marketing. Put another way, Pinduoduo has natural operating leverage in its social-based business model as it scales.

We can see the impacts of this operating leverage this year. In Q2, sales and marketing as a percentage of revenue fell eight points to 73% (whereas at the time of IPO in 2018, Pinduoduo was spending greater than 100% of revenue on sales and marketing):

Figure 3. Pinduoduo sales and marketing expense trends

Source: Pinduoduo Q2 investor presentation

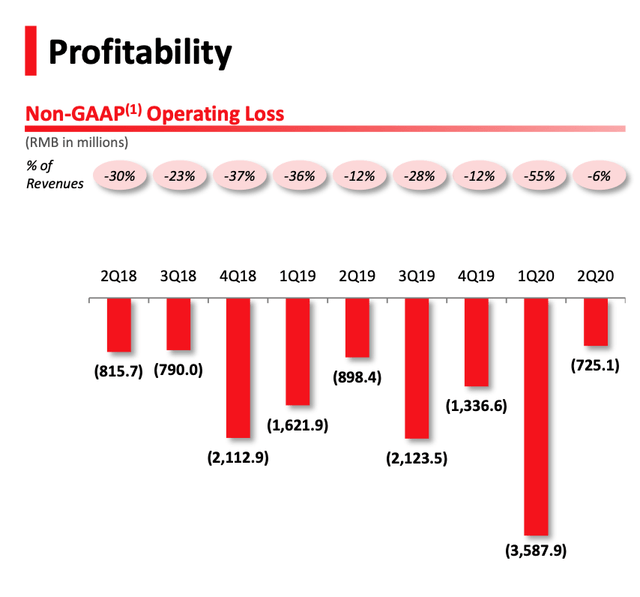

As a result, Pinduoduo has been able to squeeze down its losses. As seen in the chart below, Pinduoduo brought down its pro forma operating margins in Q2 to a near-breakeven -6%, six points better than the year-ago quarter and a far cry from the -30% margins at IPO:

Figure 4. Pinduoduo operating margin trends Source: Pinduoduo Q2 investor presentation

Source: Pinduoduo Q2 investor presentation

Key takeaways

There’s a lot to like about this fast-growing e-commerce name in China, which is little-heard of among U.S. investors. Not only does the company have an aggressive plan to continue growing its market share despite its already-large scale by addressing underpenetrated categories like agriculture, but Pinduoduo has also taken steps to march closer to profitability this year.

Look for an opportunity to carve out a long position in this stock.

For a live pulse of how tech stock valuations are moving, as well as exclusive in-depth ideas and direct access to Gary Alexander, consider subscribing to the Daily Tech Download. For as low as $17/month, you’ll get valuation comps updated daily and access to top focus list calls. This newly launched service is offering 30% off for the first 100 subscribers.

Disclosure: I am/we are long PDD. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.